17 Inference for a single mean

Focusing now on statistical inference for quantitative data, again, we will revisit and expand upon the foundational aspects of hypothesis testing from Chapters 9 and 11.

The important data structure for this chapter is a single quantitative response variable (that is, the outcome is numerical). In this and the next two chapters, the three data structures and their summary measures that we detail are:

- one quantitative response variable, summarized by a single mean,

- one quantitative response variable which is a difference across a pair of observations, summarized by a paired mean difference, and

- a quantitative response variable broken down by a binary explanatory variable, summarized by a difference in means.

When appropriate, each of the data structures will be analyzed using simulation-based inferential methods similar to those described in Chapters 9 and 10, and the theory-based methods introduced in Chapter 11.

As we build on the inferential ideas, we will visit new foundational concepts in statistical inference. One key new idea rests in estimating how the sample mean (as opposed to the sample proportion) varies from sample to sample; the resulting value is referred to as the standard error of the mean. We will also introduce a new important mathematical model, the \(t\)-distribution (as the foundation for the \(t\)-test).

To summarize a quantitative response variable, we focus on the sample mean (instead of, for example, the sample median or the range of the observations) because of the well-studied mathematical model which describes the behavior of the sample mean. The sample mean will be calculated in one group, two paired groups, and two independent groups. We will not cover mathematical models which describe other statistics, but the bootstrap and randomization techniques described below are immediately extendable to any summary measure of the observed data. The techniques described for each setting will vary slightly, but you will be well served to find the structural similarities across the different settings.

Similar to how we can model the behavior of the sample proportion \(\hat{p}\) using a normal distribution, the sample mean \(\bar{x}\) can also be modeled using a normal distribution when certain conditions are met. However, we’ll soon learn that a new distribution, called the \(t\)-distribution, tends to be more useful when working with the sample mean. We’ll first learn about this new distribution, then we’ll use it to construct confidence intervals and conduct hypothesis tests for the mean.

Below we summarize the notation used throughout this chapter.

Notation for a single quantitative variable.

- \(n\) = sample size

- \(\bar{x}\) = sample mean

- \(s\) = sample standard deviation

- \(\mu\) = population mean

- \(\sigma\) = population standard deviation

A single mean is used to summarize data when we measured a single quantitative variable on each observational unit, e.g., GPA, age, salary. Aside from slight differences in notation, the inferential methods presented in this section will be identical to those for a paired mean difference, as we will see in Chapter 18.

17.1 Bootstrap confidence interval for \(\mu\)

In this section, we will use bootstrapping, first introduced in Chapter 10, to construct a confidence interval for a population mean. Recall that bootstrapping is best suited for modeling studies where the data have been generated through random sampling from a population. Our bootstrapped distribution of sample means will mimic the process of randomly sampling from a population to give us a sense of how sample means will vary from sample to sample.

17.1.1 Observed data

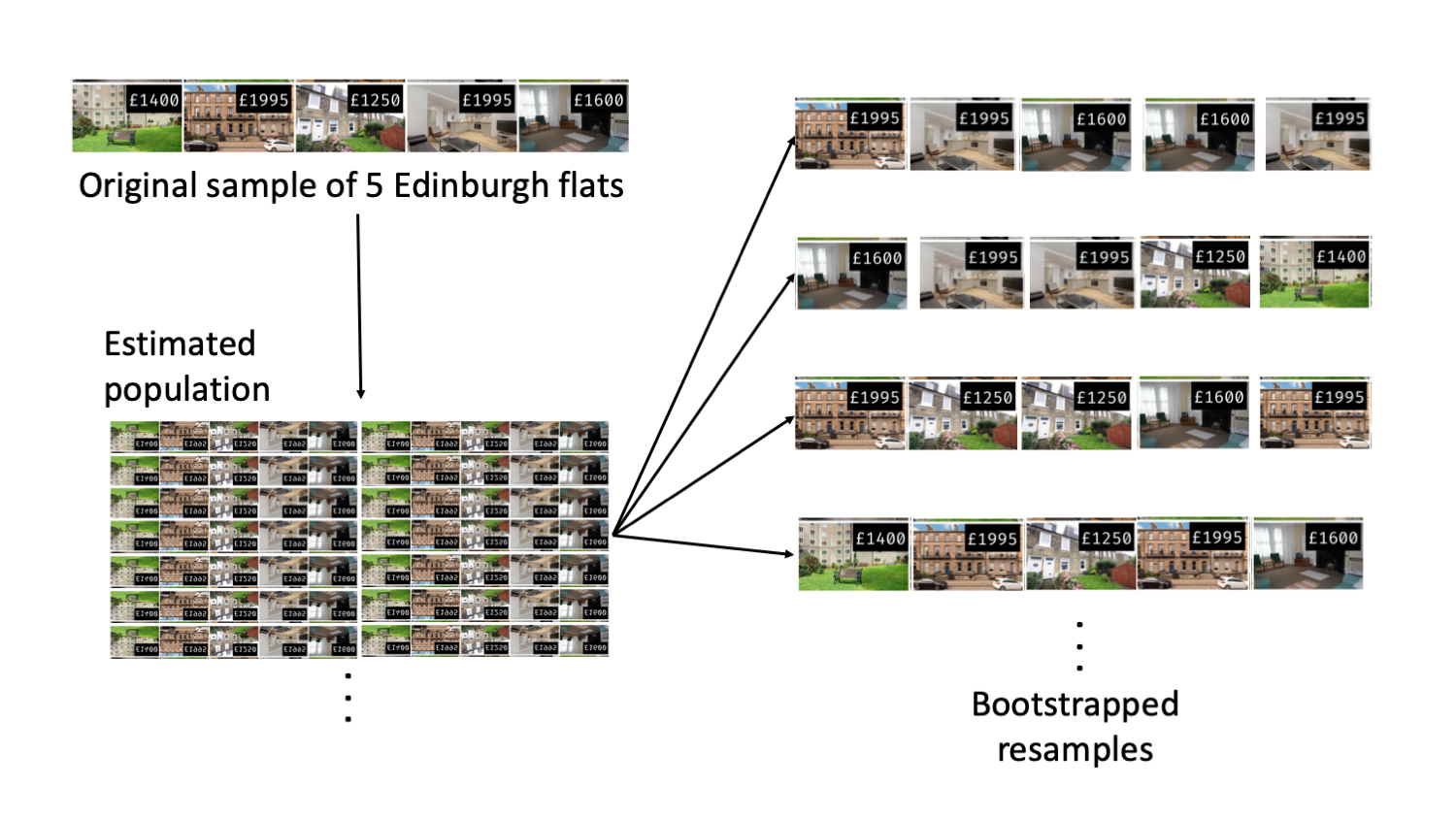

As an employer who subsidizes housing for your employees, you need to know the average monthly rental price for a three bedroom flat in Edinburgh. In order to walk through the example more clearly, let’s say that you are only able to randomly sample five Edinburgh flats (if this were a real example, you would surely be able to take a much larger sample size, possibly even being able to measure the entire population!).

Figure 17.1 presents the details of the random sample of observations where the monthly rent of five flats has been recorded.

Figure 17.1: Five randomly sampled flats in Edinburgh.

The sample average monthly rent of £1648 is a first guess at the price of three bedroom flats. However, as a student of statistics, you understand that one sample mean based on a sample of five observations will not necessarily equal the true population average rent for all three bedroom flats in Edinburgh. Indeed, you can see that the observed rent prices vary with a standard deviation of £340.232, and surely the average monthly rent would be different if a different sample of size five had been taken from the population. Fortunately, we can use bootstrapping to approximate the variability of the sample mean from sample to sample.

17.1.2 Variability of the statistic

As with the inferential ideas covered in previous chapters, the inferential analysis methods in this chapter are grounded in quantifying how one data set differs from another when they are both taken from the same population.

Figure 17.2 shows how the unknown original population of all three bedroom flats in Edinburgh can be estimated by using many duplicates of the sample. This estimated population—consisting of infinitely many copies of the original sample—can then be used to generate bootstrapped resamples.

Figure 17.2: Using the original sample of five Edinburgh flats to generate an estimated population, which is then used to generate bootstrapped resamples. This process of generating a bootstrapped sample is equivalent to sampling five flats from the original sample, with replacement.

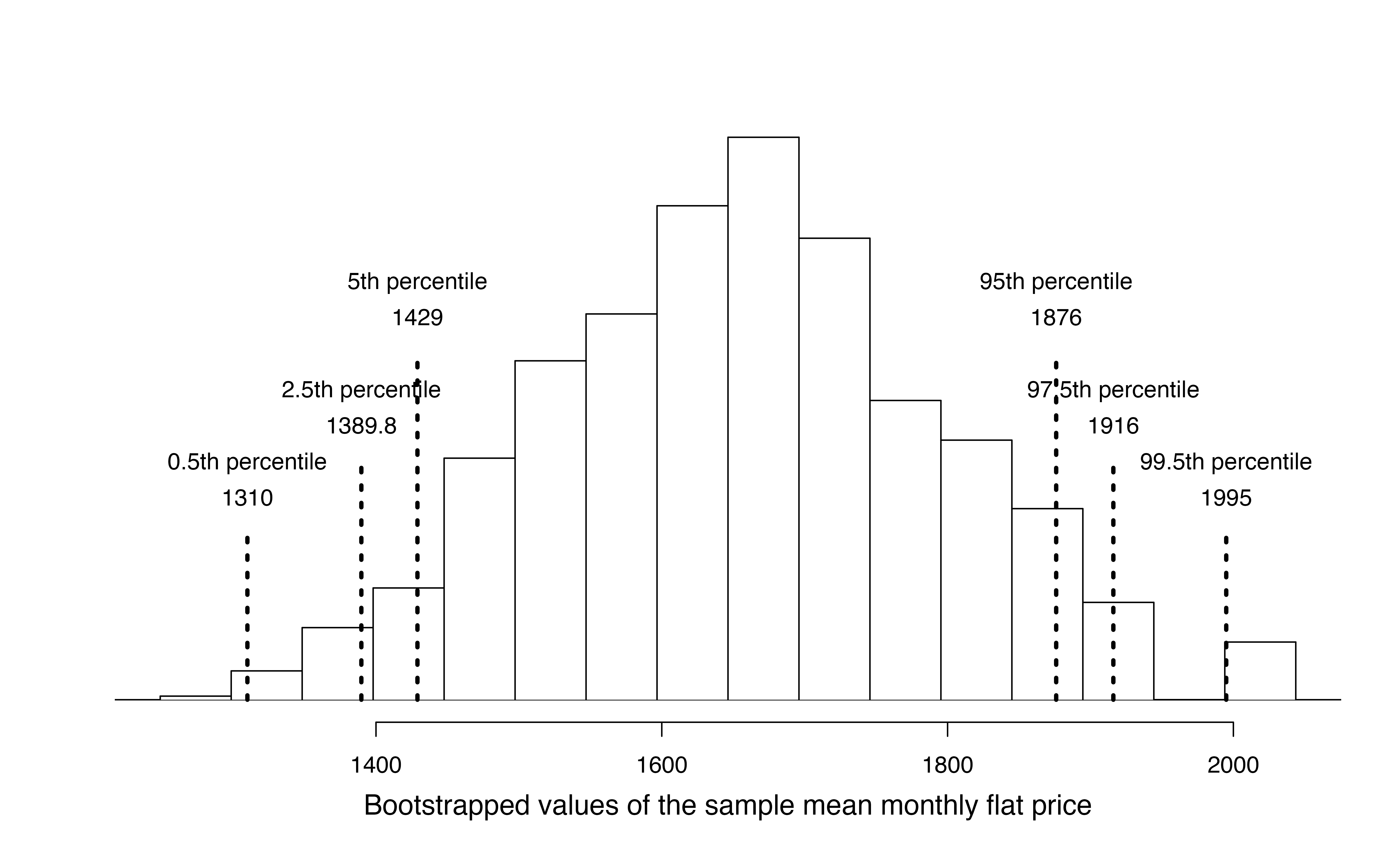

In Figure 17.2, the repeated bootstrap resamples are obviously different both from each other and from the original sample. Since the bootstrap resamples are taken from the same (estimated) population, these differences are due entirely to natural variability in the sampling procedure. By summarizing each of the bootstrap resamples (here, using the sample mean), we see, directly, the variability of the sample mean from sample to sample. The distribution of \(\bar{x}_{boot}\), the bootstrapped sample means, for the Edinburgh flats is shown in Figure 17.3.

Figure 17.3: Distribution of bootstrapped means from 1,000 simulated bootstrapped samples generated by sampling with replacement from our original sample of five Edinburgh flats. The histogram provides a sense for the variability of the average rent values from sample to sample for samples of size 5.

The bootstrapped average rent prices vary from £1250 to £1995 (with a small observed sample of size 5, a bootstrap resample can sometimes, although rarely, include only repeated measurements of the same observation).

Bootstrapping from one sample.

- Take a random sample of size \(n\) from the original sample, with replacement. This is called a bootstrapped resample.

- Record the sample mean (or statistic of interest) from the bootstrapped resample. This is called a bootstrapped statistic.

- Repeat steps (1) and (2) 1000s of times.

Due to theory that is beyond this text, we know that the bootstrap means \(\bar{x}_{boot}\) vary around the original sample mean, \(\bar{x}\), in a similar way to how different sample (i.e., different data sets which would produce different \(\bar{x}\) values) means vary around the true parameter \(\mu\). Therefore, an interval estimate for \(\mu\) can be produced using the \(\bar{x}_{boot}\) values themselves. A 95% bootstrap confidence interval for \(\mu\), the population mean rent price for three bedroom flats in Edinburgh, is found by locating the middle 95% of the bootstrapped sample means in Figure 17.3.

95% Bootstrap confidence interval for a population mean \(\mu\).

The 95% bootstrap confidence interval for the parameter \(\mu\) can be obtained directly using the ordered values \(\bar{x}_{boot}\) values — the bootstrapped sample means. Consider the sorted \(\bar{x}_{boot}\) values, and let \(\bar{x}_{boot, 0.025}\) be the 2.5th percentile and \(\bar{x}_{boot, 0.025}\) be the 97.5th percentile. The 95% confidence interval is given by:You can find confidence intervals of difference confidence levels by changing the percent of the distribution you take, e.g., locate the middle 90% of the bootstrapped statistics for a 90% confidence interval.

Using Figure 17.3, find the 90% and 95% confidence intervals for the true mean monthly rental price of a three bedroom flat in Edinburgh.

A 90% confidence interval is given by (£1429, £1876). The conclusion is that we are 90% confident that the true average rental price for three bedroom flats in Edinburgh lies somewhere between £1429 and £1876.

A 95% confidence interval is given by (£1389.75, £1916). The conclusion is that we are 95% confident that the true average rental price for three bedroom flats in Edinburgh lies somewhere between £1389.75 and £1916.

17.1.3 Bootstrap percentile confidence interval for \(\sigma\) (special topic)

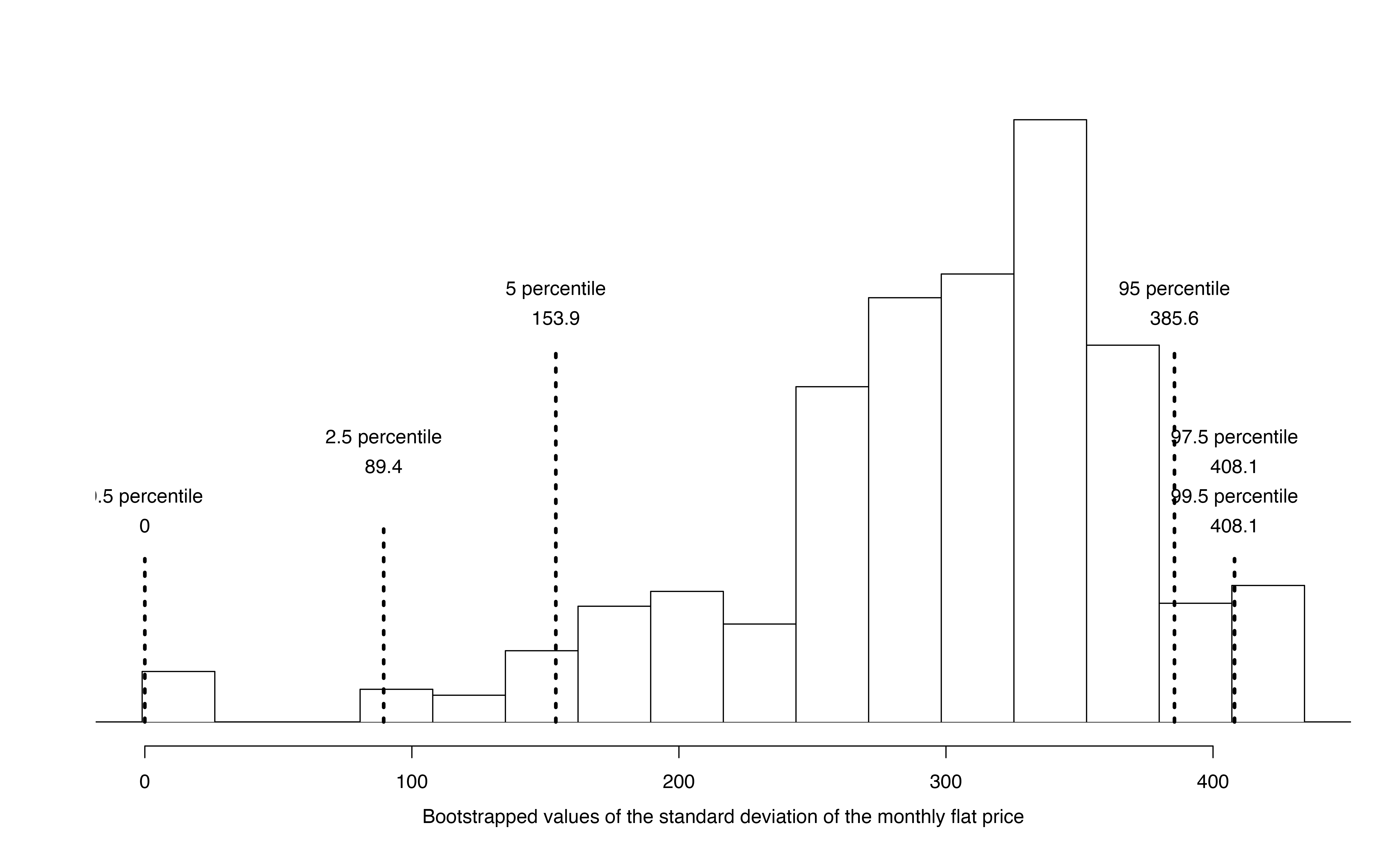

Suppose that the research question at hand seeks to understand how variable the rental price of the three bedroom flats are in Edinburgh. That is, your interest is no longer in the average rental price of the flats but in the standard deviation of the rental prices of all three bedroom flats in Edinburgh, \(\sigma\). You may have already realized that the sample standard deviation, \(s\), will work as a good point estimate for the parameter of interest: the population standard deviation, \(\sigma\). The point estimate of the five observations is calculated to be \(s =\) £340.23. While \(s =\) £340.23 might be a good guess for \(\sigma\), we prefer to have an interval. Although there is a mathematical model which describes how \(s\) varies from sample to sample, the mathematical model will not be presented in this text. But even without the mathematical model, bootstrapping can be used to find a confidence interval for the parameter \(\sigma\).

Describe the bootstrap distribution for the standard deviation shown in Figure 17.4.

The distribution is skewed left and centered near £340.23, which is the point estimate from the original data. Most observations in this distribution lie between £0 and £408.1.

Using Figure 17.4, find and interpret a 90% confidence interval for the population standard deviation for three bedroom flat prices in Edinburgh.143

Figure 17.4: The original Edinburgh data is bootstrapped 1,000 times. The histogram provides a sense for the variability of the standard deviation of the rent values from sample to sample.

17.1.4 Bootstrapping is not a solution to small sample sizes!

The example presented above is done for a sample with only five observations. As with analysis techniques that build on mathematical models, bootstrapping works best when a large random sample has been taken from the population. Bootstrapping is a method for capturing the variability of a statistic when the mathematical model is unknown — it is not a method for navigating small samples. As you might guess, the larger the random sample, the more accurately that sample will represent the target population.

17.2 Shifted bootstrap test for \(H_0: \mu = \mu_0\)

We can also use bootstrapping to conduct a simulation-based test of the null hypothesis that the population mean is equal to a specified value, \(\mu_0\), called the null value. In this case, we first shift each value in the data set so that the sample distribution is centered at \(\mu_0\). Then, we bootstrap from the shifted data in order to generate a null distribution of sample means. Consider the following example.

In 1851, Carl Wunderlich, a German physician, measured body temperatures of around 25,000 adults and found that the average body temperature was 98.6\(^{\circ}\)F, which we’ve believed ever since. However, a recent study conducted at Stanford University suggests that the average body temperature may actually be lower than 98.6\(^{\circ}\)F.144

17.2.1 Observed data

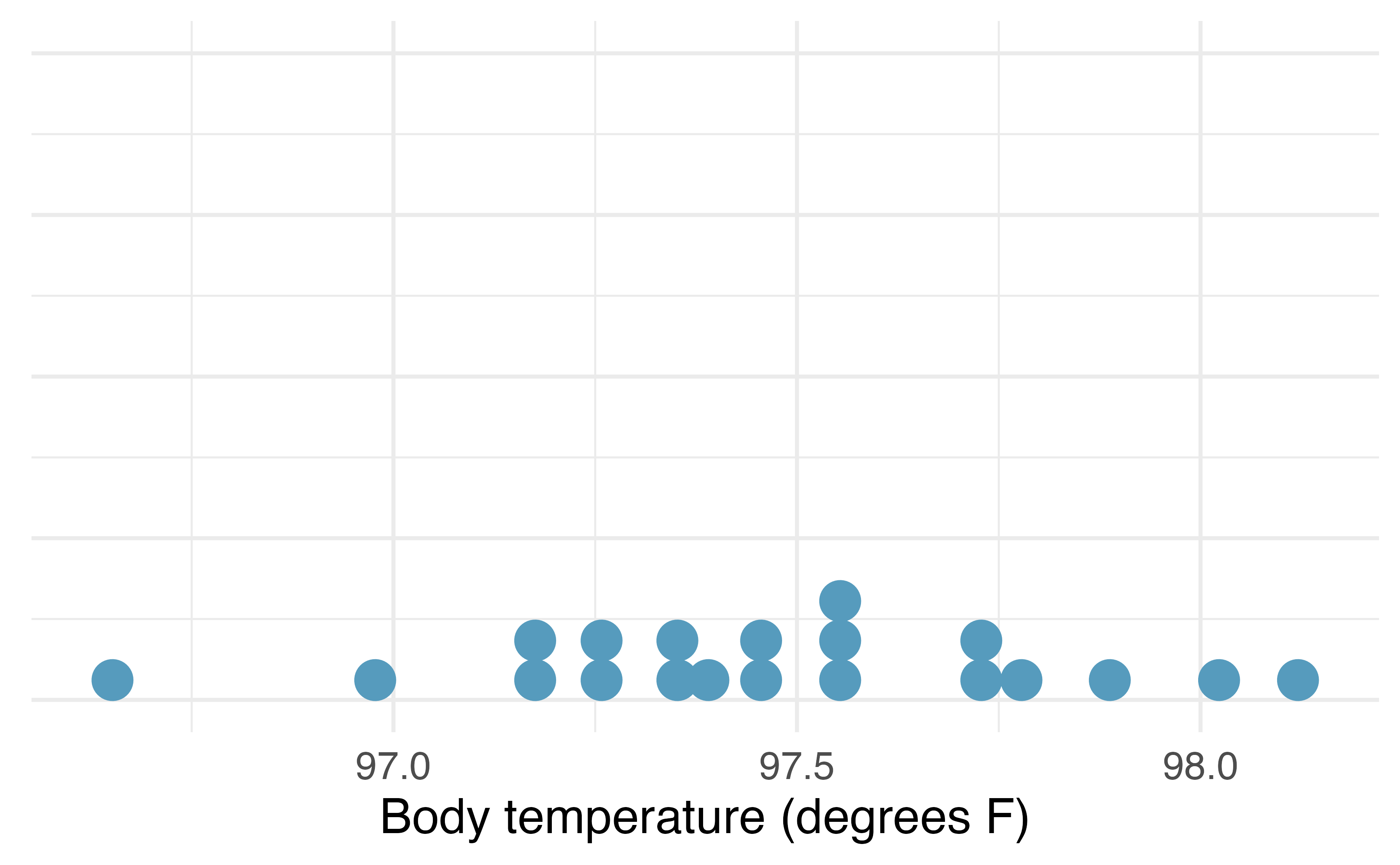

Curious if average body temperature has decreased since 1851, you decided to collect data on a random sample of twenty Montana State University students. The mean body temperature in your sample is \(\bar{x}\) = 97.47\(^{\circ}\)F, and the standard deviation is \(s\) = 0.35\(^{\circ}\)F. A dot plot of the data is shown in Figure 17.5, with summary statistics displayed below.

favstats(temperatures)#> min Q1 median Q3 max mean sd n missing

#> 96.7 97.3 97.5 97.7 98.1 97.5 0.353 20 0

Figure 17.5: Distribution of body temperatures in a random sample of twenty Montana State University students.

17.2.2 Shifted bootstrapped null distribution

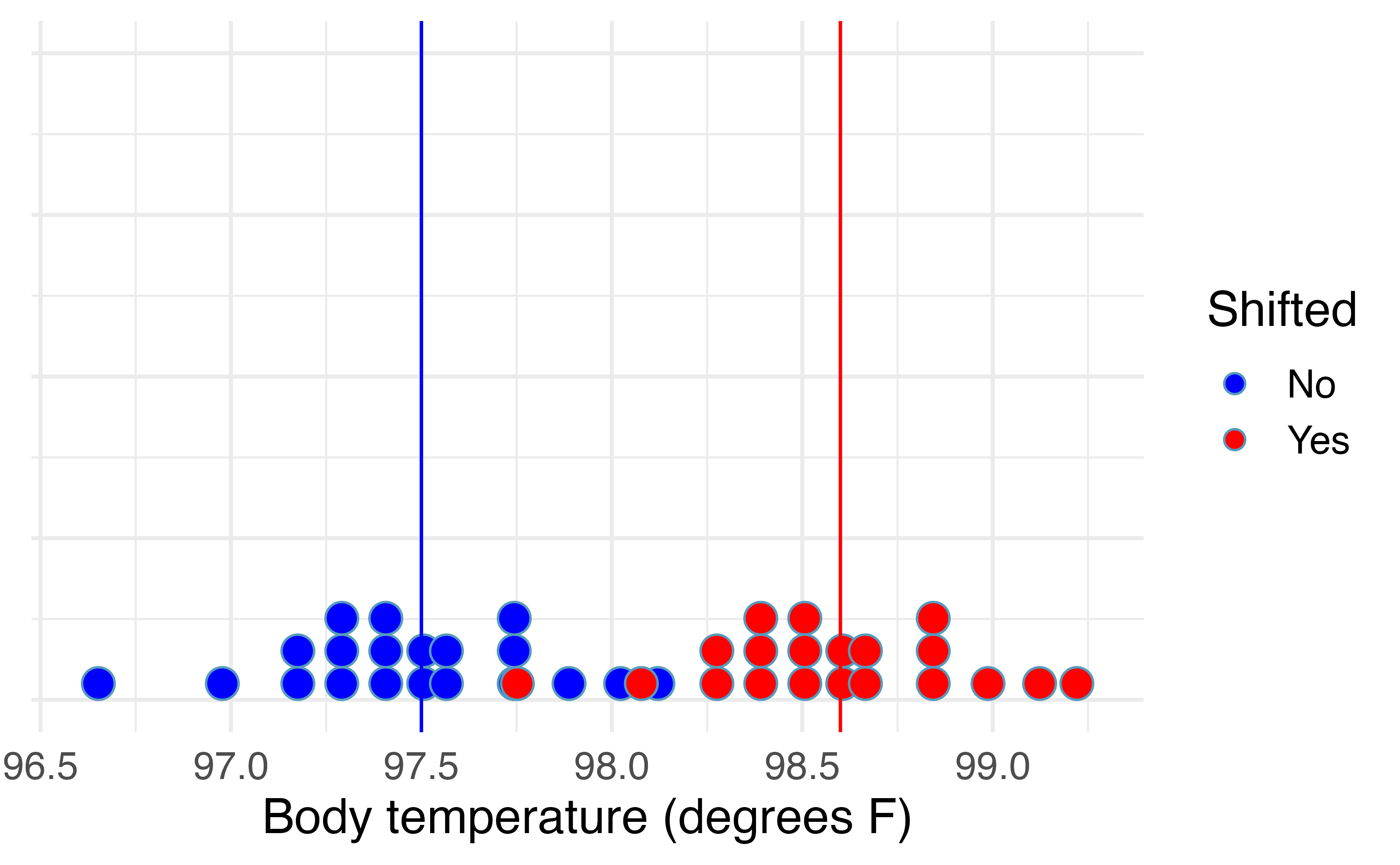

We would like to test the set of hypotheses \(H_0: \mu = 98.6\) versus \(H_A: \mu < 98.6\), where \(\mu\) is the true mean body temperature among all adults (in degrees F). If we were to simulate sample mean body temperatures under \(H_0\), we would expect the null distribution to be centered at \(\mu_0\) = 98.6\(^\circ\)F. However, if we bootstrap sample means from our observed sample, the bootstrap distribution will be centered at the sample mean body temperature \(\bar{x}\) = 97.5\(^\circ\)F.

To use bootstrapping to generate a null distribution of sample means, we first have to shift the data to be centered at the null value. We do this by adding \(\mu_0 - \bar{x} = 98.6 - 97.5 = 1.1^\circ\)F to each body temperature in the sample. This process is displayed in Figure 17.6.

Figure 17.6: Distribution of body temperatures in a random sample of twenty Montana State University students (blue) and the shifted body temperatures (red), found by adding 1.1 degree F to each original body temperature.

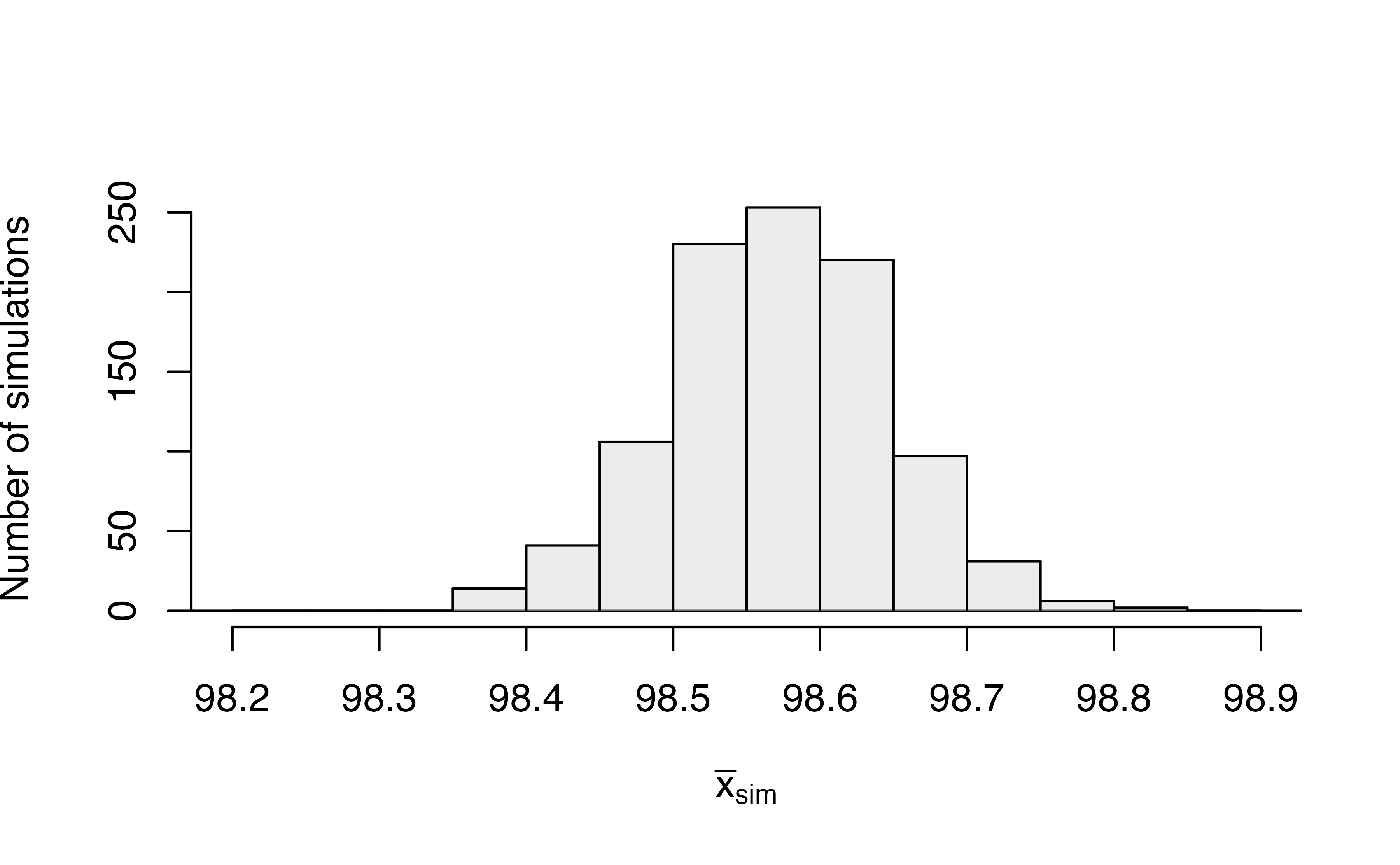

A bootstrapped null distribution generated from sampling 20 shifted temperatures, with replacement, from the shifted data 1,000 times is shown in Figure 17.7.

Figure 17.7: Bootstrapped null distribution of sample mean temperatures assuming the true mean temperature is 98.6 degrees F.

Shifted bootstrap null distribution for a sample mean.

To simulate a null distribution of sample means under the null hypothesis \(H_0: \mu = \mu_0\):

- Add \(\mu_0 - \bar{x}\) to each value in the original sample: \[ x_1 + \mu_0 - \bar{x}, \hspace{2.5mm} x_2 + \mu_0 - \bar{x}, \hspace{2.5mm} x_3 + \mu_0 - \bar{x}, \hspace{2.5mm} \ldots, \hspace{2.5mm} x_n + \mu_0 - \bar{x}. \] Note that if \(\bar{x}\) is larger than \(\mu\), then the quantity \(\mu_0 - \bar{x}\) will be negative, and you will be subtracting the distance between \(\mu\) and \(\bar{x}\) from each value.

- Generate 1000s of bootstrap resamples from this shifted distribution, plotting the shifted bootstrap sample mean each time.

To calculate the p-value, since \(H_A: \mu < 98.6\), we find the proportion of simulated sample means that were less than or equal to our original sample mean, \(\bar{x}\) = 97.47. As shown in Figure 17.7, none of our simulated sample means were 97.5\(^\circ\)F or lower, giving us very strong evidence that the true mean body temperature among all Montana State University students is less than the commonly accepted 98.6\(^\circ\)F average temperature.

17.3 Theory-based inferential methods for \(\mu\)

As with the sample proportion, the variability of the sample mean is well described by the mathematical theory given by the Central Limit Theorem. Similar to how we can model the behavior of the sample proportion \(\hat{p}\) using a normal distribution, the sample mean \(\bar{x}\) can also be modeled using a normal distribution when certain conditions are met. However, because of missing information about the inherent variability in the population, a \(t\)-distribution is used in place of the standard normal when performing hypothesis test or confidence interval analyses.

Central Limit Theorem for the sample mean.

When we collect a sufficiently large sample of

\(n\) independent observations from a population with

mean \(\mu\) and standard deviation \(\sigma\),

the sampling distribution of \(\bar{x}\) will be nearly

normal with

\[\begin{align*}

&\text{Mean}=\mu

&&\text{Standard Deviation }(SD) = \frac{\sigma}{\sqrt{n}}

\end{align*}\]

Before diving into confidence intervals and hypothesis tests using \(\bar{x}\), we first need to cover two topics:

- When we modeled \(\hat{p}\) using the normal distribution, certain conditions had to be satisfied. The conditions for working with \(\bar{x}\) are a little more complex, and below, we will discuss how to check conditions for inference using a mathematical model.

- The standard deviation of the sample mean is dependent on the population standard deviation, \(\sigma\). However, we rarely know \(\sigma\), and instead we must estimate it. Because this estimation is itself imperfect, we use a new distribution called the \(t\)-distribution to fix this problem.

17.3.1 Evaluating the two conditions required for modeling \(\bar{x}\) using theory-based methods

There are two conditions required to apply the Central Limit Theorem for a sample mean \(\bar{x}\). When the sample observations are independent and the sample size is sufficiently large, the normal model will describe the variability in sample means quite well; when the observations violate the conditions, the normal model can be inaccurate.

Conditions for the modeling \(\bar{x}\) using theory-based methods.

The sampling distribution for \(\bar{x}\) based on a sample of size \(n\) from a population with a true mean \(\mu\) and true standard deviation \(\sigma\) can be modeled using a normal distribution when:

Independence. The sample observations must be independent, The most common way to satisfy this condition is when the sample is a simple random sample from the population. If the data come from a random process, analogous to rolling a die, this would also satisfy the independence condition.

-

Normality. When a sample is small, we also require that the sample observations come from a normally distributed population. We can relax this condition more and more for larger and larger sample sizes. This condition is obviously vague, making it difficult to evaluate, so next we introduce a couple rules of thumb to make checking this condition easier.

When these conditions are satisfied, then the sampling distribution of \(\bar{x}\) is approximately normal with mean \(\mu\) and standard deviation \(\frac{\sigma}{\sqrt{n}}\).

General rule: how to perform the normality check.

There is no perfect way to check the normality condition, so instead we use the following general rules:

-

\(\mathbf{n < 30}\): If the sample size \(n\) is less than 30

and there are no clear outliers in the data,

then we typically assume the data come from

a nearly normal distribution to satisfy the

condition.

- \(\mathbf{n \geq 30}\): If the sample size \(n\) is at least 30 and there are no particularly extreme outliers, then we typically assume the sampling distribution of \(\bar{x}\) is nearly normal, even if the underlying distribution of individual observations is not.

- \(\mathbf{n > 100}\): If the sample size \(n\) is at least 100 (regardless of the presence of skew or outliers), we typically assume the sampling distribution of \(\bar{x}\) is nearly normal, even if the underlying distribution of individual observations is not.

In this first course in statistics, you aren’t expected to develop perfect judgement on the normality condition. However, you are expected to be able to handle clear cut cases based on the rules of thumb above.

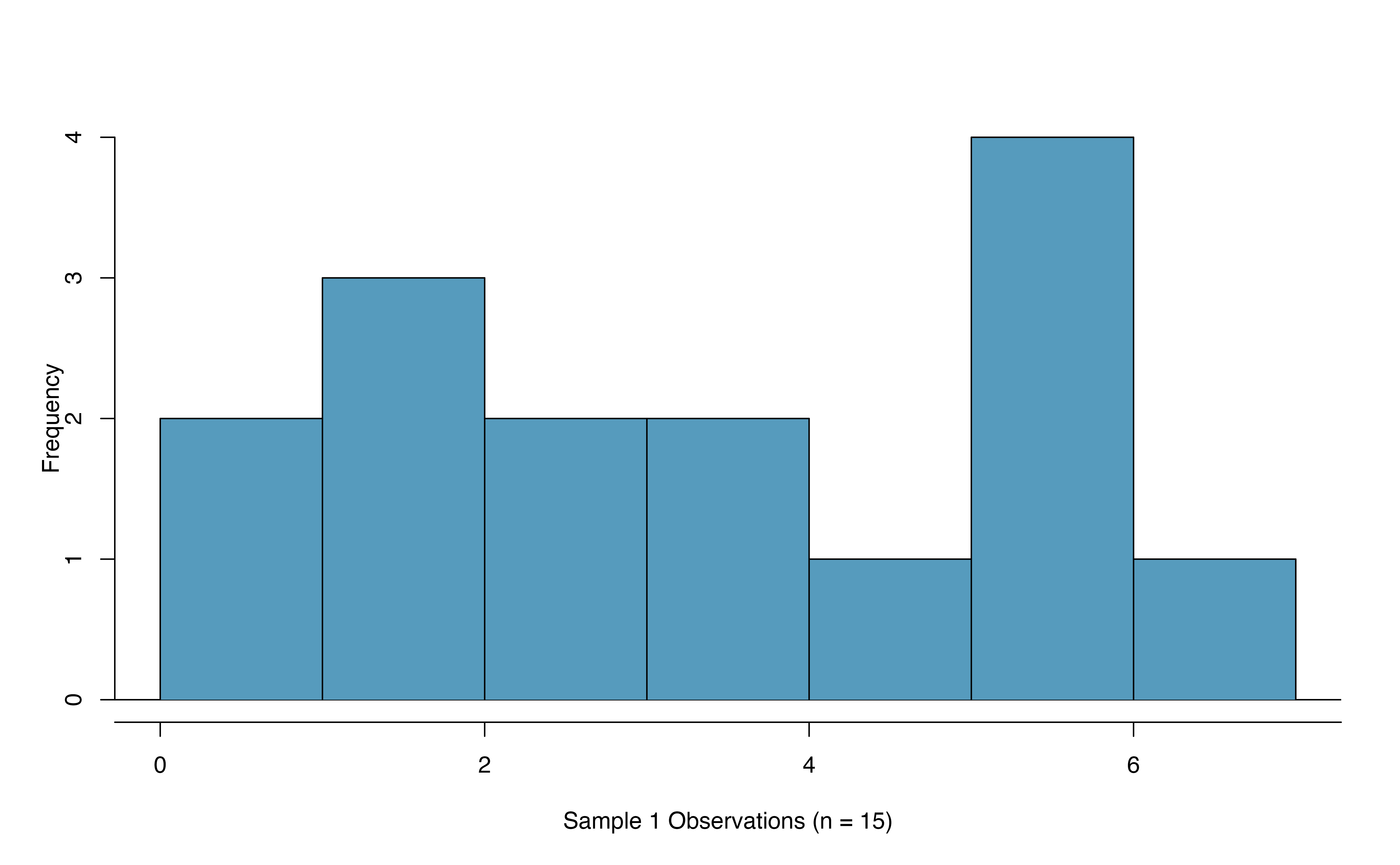

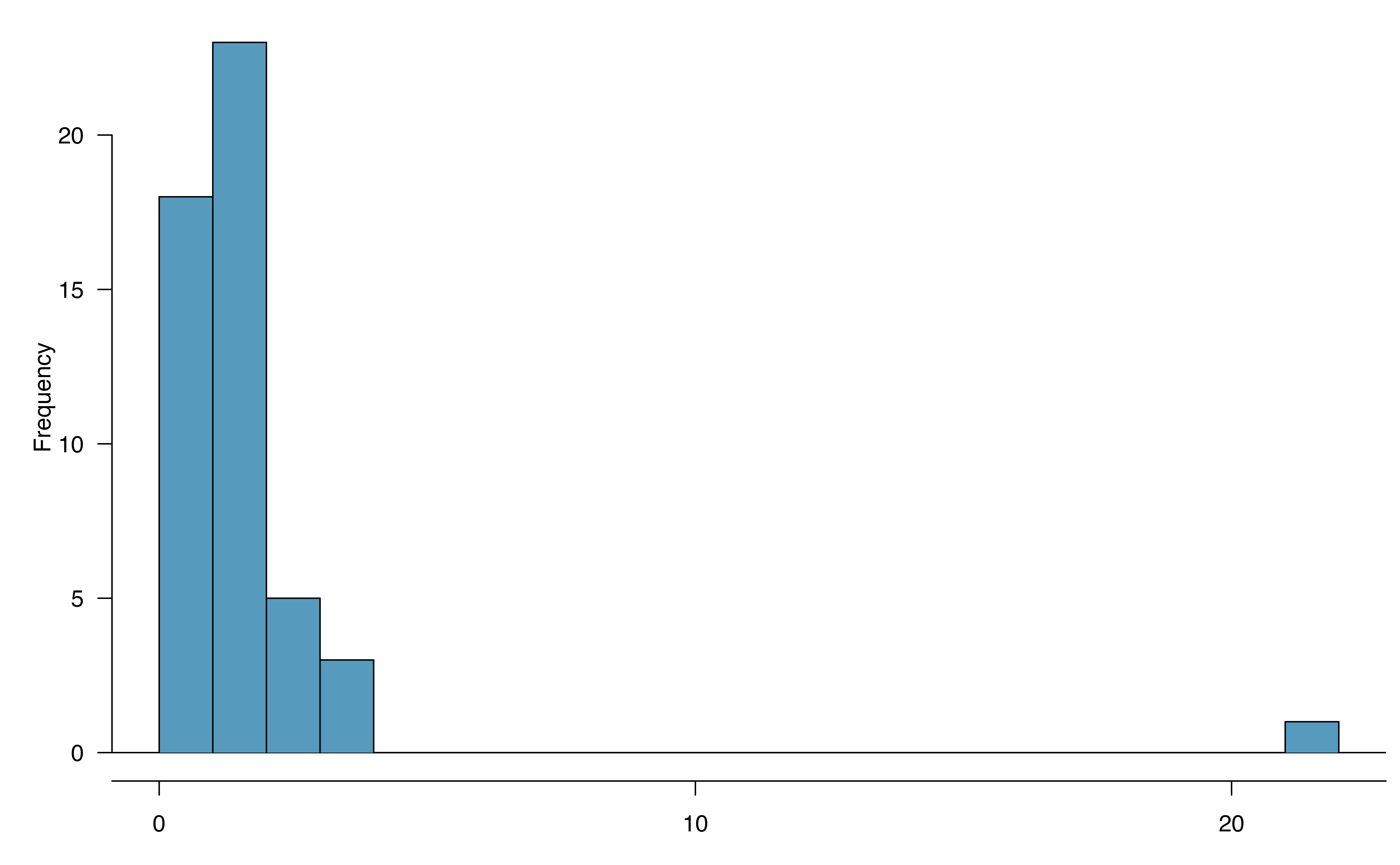

Example 17.1 Consider the following two plots that come from simple random samples from different populations. Their sample sizes are \(n_1 = 15\) and \(n_2 = 50\).

Are the independence and normality conditions met in each case?

Each sample is from a simple random sample of its respective population, so the independence condition is satisfied. Let’s next check the normality condition for each using the rule of thumb.

The first sample has fewer than 30 observations, so we are watching for any clear outliers. None are present; while there is a small gap in the histogram on the right, this gap is small and 20% of the observations in this small sample are represented in that far right bar of the histogram, so we can hardly call these clear outliers. With no clear outliers, the normality condition is reasonably met.

The second sample has a sample size greater than 30 and includes an outlier that appears to be roughly 5 times further from the center of the distribution than the next furthest observation. This is an example of a particularly extreme outlier, so the normality condition would not be satisfied.

In practice, it’s typical to also do a mental check to evaluate whether we have reason to believe the underlying population would have moderate skew (if \(n < 30\)) or have particularly extreme outliers \((n \geq 30)\) beyond what we observe in the data. For example, consider the number of followers for each individual account on Twitter, and then imagine this distribution. The large majority of accounts have built up a couple thousand followers or fewer, while a relatively tiny fraction have amassed tens of millions of followers, meaning the distribution is extremely skewed. When we know the data come from such an extremely skewed distribution, it takes some effort to understand what sample size is large enough for the normality condition to be satisfied.

17.3.2 Introducing the \(t\)-distribution

In practice, we cannot directly calculate the standard deviation for \(\bar{x}\) since we do not know the population standard deviation, \(\sigma\). We encountered a similar issue when computing the standard error for a sample proportion, which relied on the population proportion, \(\pi\). Our solution in the proportion context was to use sample value in place of the population value to calculate a standard error. We’ll employ a similar strategy to compute the standard error of \(\bar{x}\), using the sample standard deviation \(s\) in place of \(\sigma\): \[\begin{align*} SE(\bar{x}) = \frac{s}{\sqrt{n}} \approx SD(\bar{x}) = \frac{\sigma}{\sqrt{n}}. \end{align*}\] The standard error of \(\bar{x}\) provides an estimate of the standard deviation of \(\bar{x}\). This strategy tends to work well when we have a lot of data and can estimate \(\sigma\) using \(s\) accurately. However, the estimate is less precise with smaller samples, and this leads to problems when using the normal distribution to model \(\bar{x}\) if we do not know \(\sigma\).

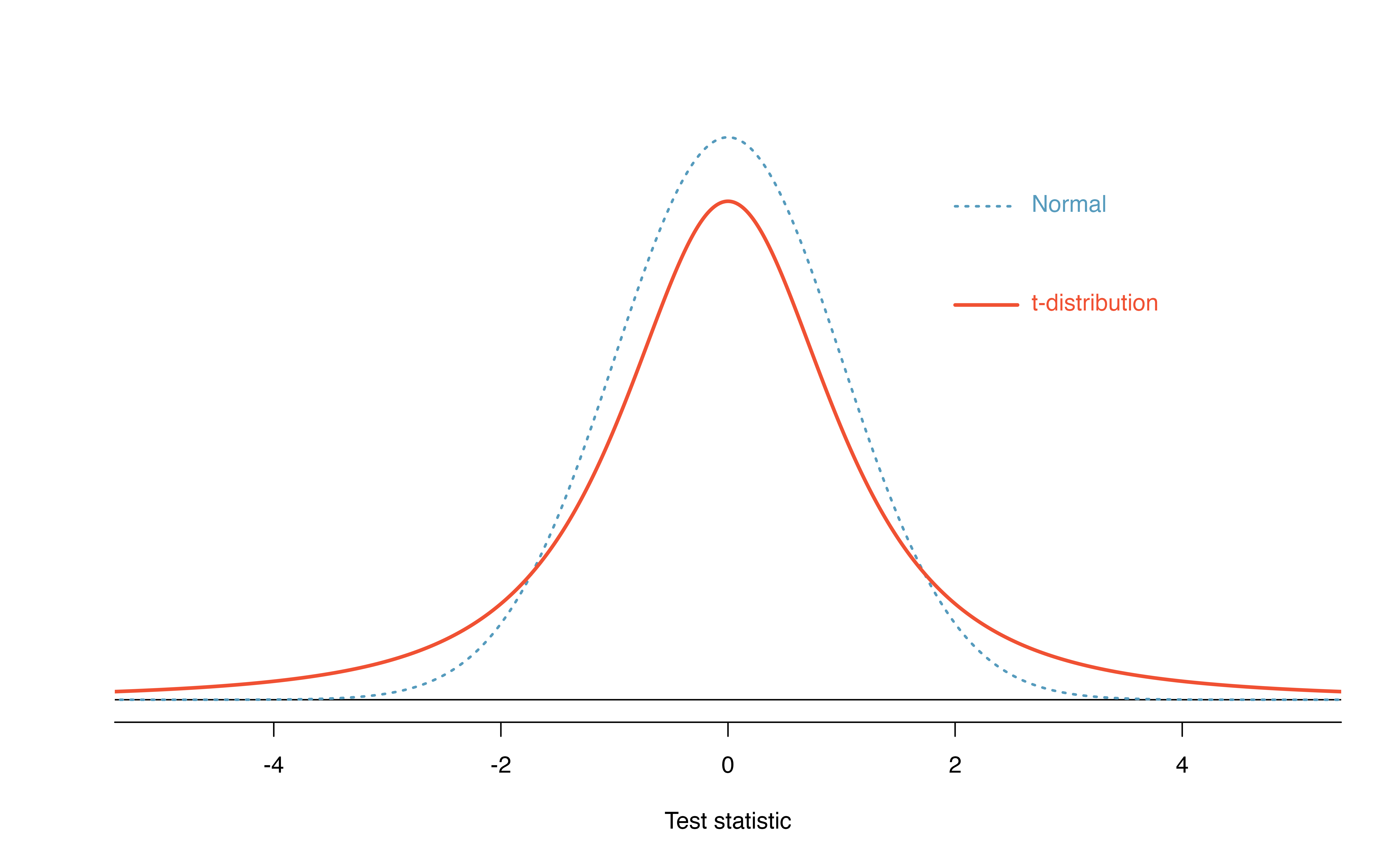

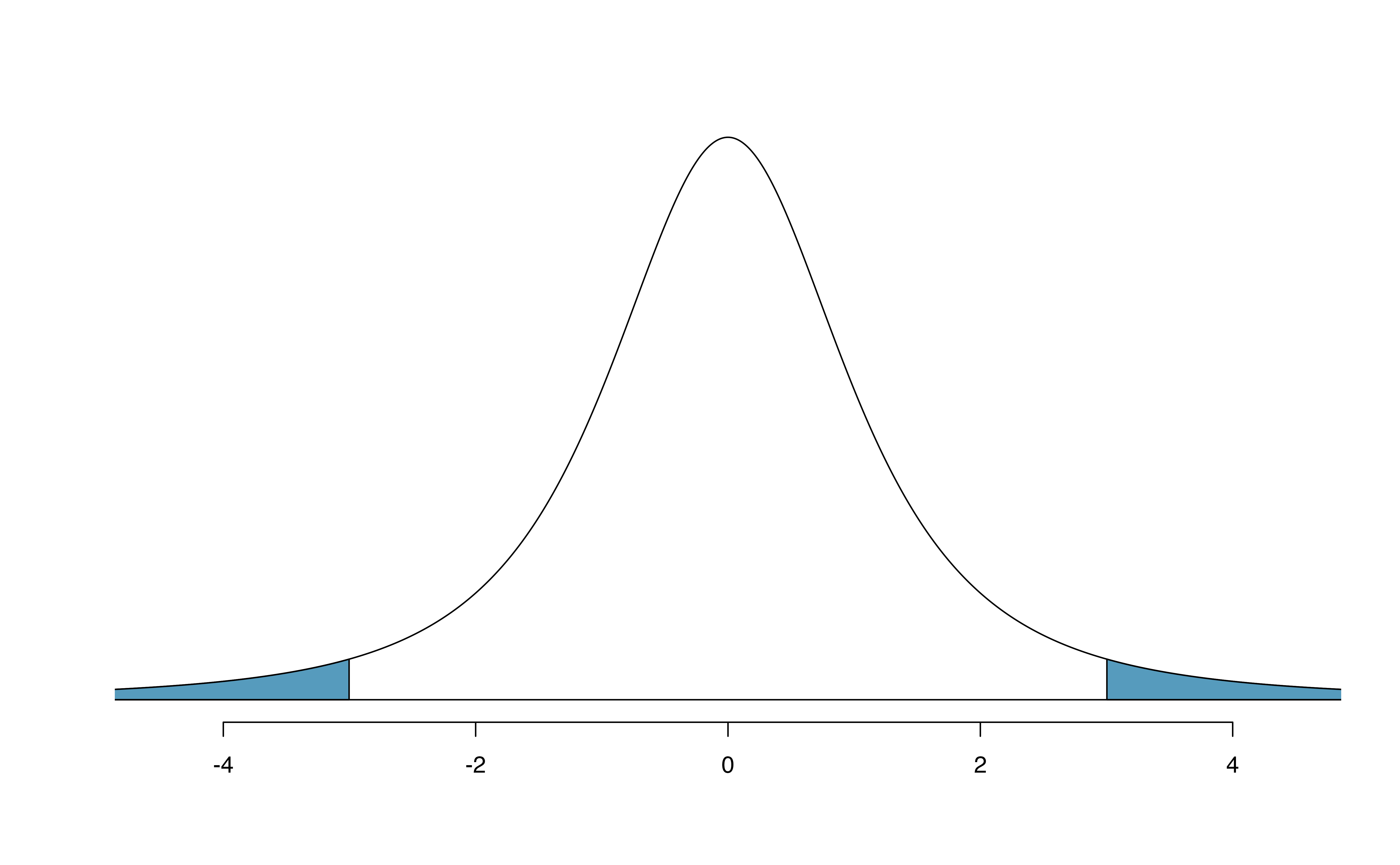

We’ll find it useful to use a new distribution for inference calculations called the \(t\)-distribution. A \(t\)-distribution, shown as a solid line in Figure 17.8, has a bell shape. However, its tails are thicker than the normal distribution’s, meaning observations are more likely to fall beyond two standard deviations from the mean than under the normal distribution.

The extra thick tails of the \(t\)-distribution are exactly the correction needed to resolve the problem (due to extra variability of the test statistic) of using \(s\) in place of \(\sigma\) in the \(SE(\bar{x})\) calculation.

Figure 17.8: Comparison of a \(t\)-distribution and a normal distribution.

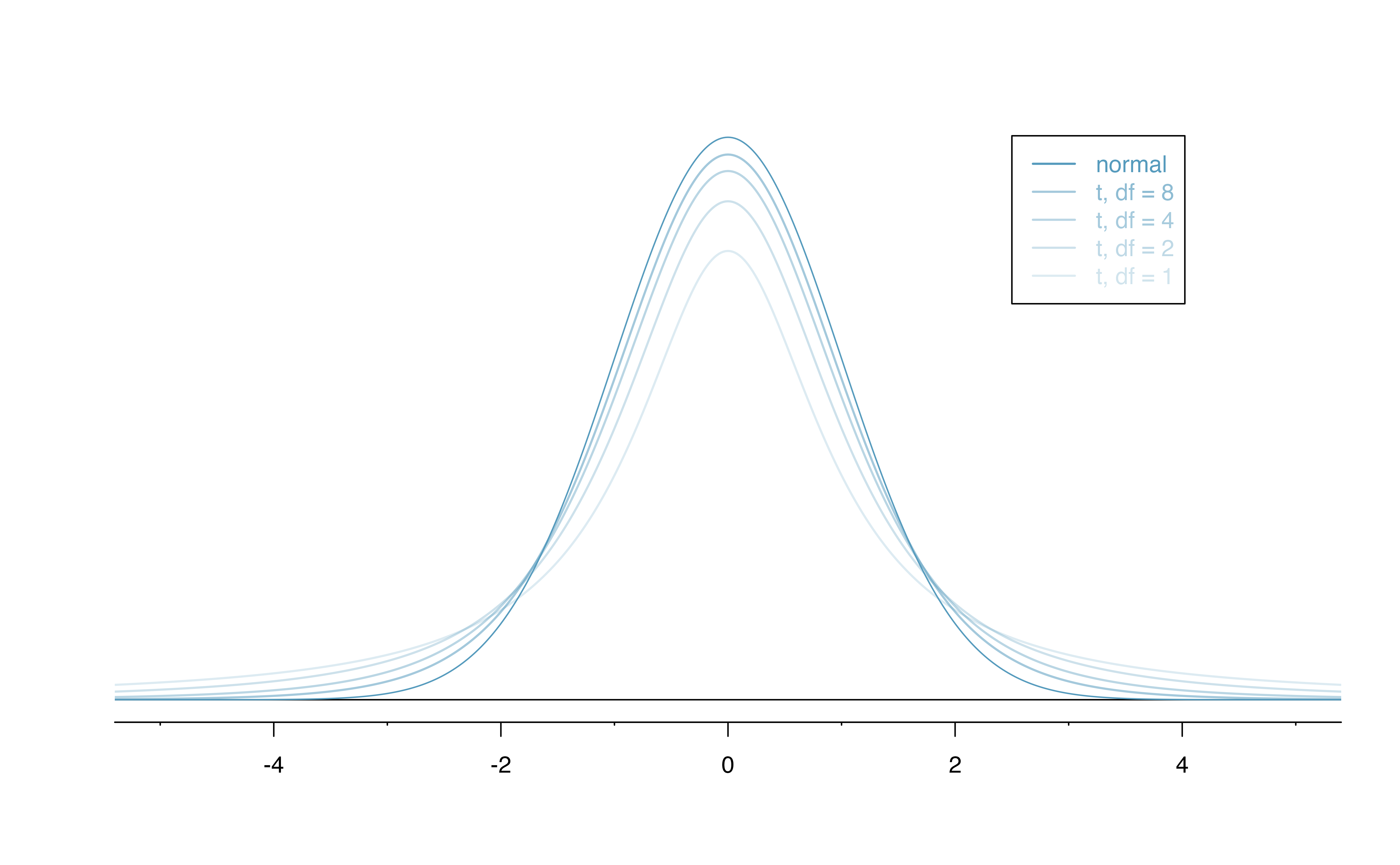

The \(t\)-distribution is always centered at zero and has a single parameter: degrees of freedom (\(df\)). The degrees of freedom describes the precise form of the bell-shaped \(t\)-distribution. Several \(t\)-distributions are shown in Figure 17.9 in comparison to the normal distribution.

For inference with a single mean, we’ll use a \(t\)-distribution with \(df = n - 1\) to model the sample mean when the sample size is \(n\). That is, when we have more observations, the degrees of freedom will be larger and the \(t\)-distribution will look more like the standard normal distribution; when the degrees of freedom is about 30 or more, the \(t\)-distribution is nearly indistinguishable from the normal distribution.

Figure 17.9: The larger the degrees of freedom, the more closely the \(t\)-distribution resembles the standard normal distribution.

Degrees of freedom: \(df\).

The degrees of freedom describes the shape of the \(t\)-distribution. The larger the degrees of freedom, the more closely the distribution approximates the normal model.

When modeling \(\bar{x}\) using the \(t\)-distribution, use \(df = n - 1\).

The \(t\)-distribution allows us greater flexibility than

the normal distribution when analyzing numerical data.

In practice, it’s common to use statistical software,

such as R, Python, or SAS for these analyses.

In R, the function used for calculating probabilities under a \(t\)-distribution is pt() (which should seem similar to the previous R function pnorm()).

Don’t forget that with the \(t\)-distribution, the degrees of freedom must always be specified!

For the examples and guided practices below, use R to find the answers. We recommend trying the problems so as to get a sense for how the \(t\)-distribution can vary in width depending on the degrees of freedom, and to confirm your working understanding of the \(t\)-distribution.

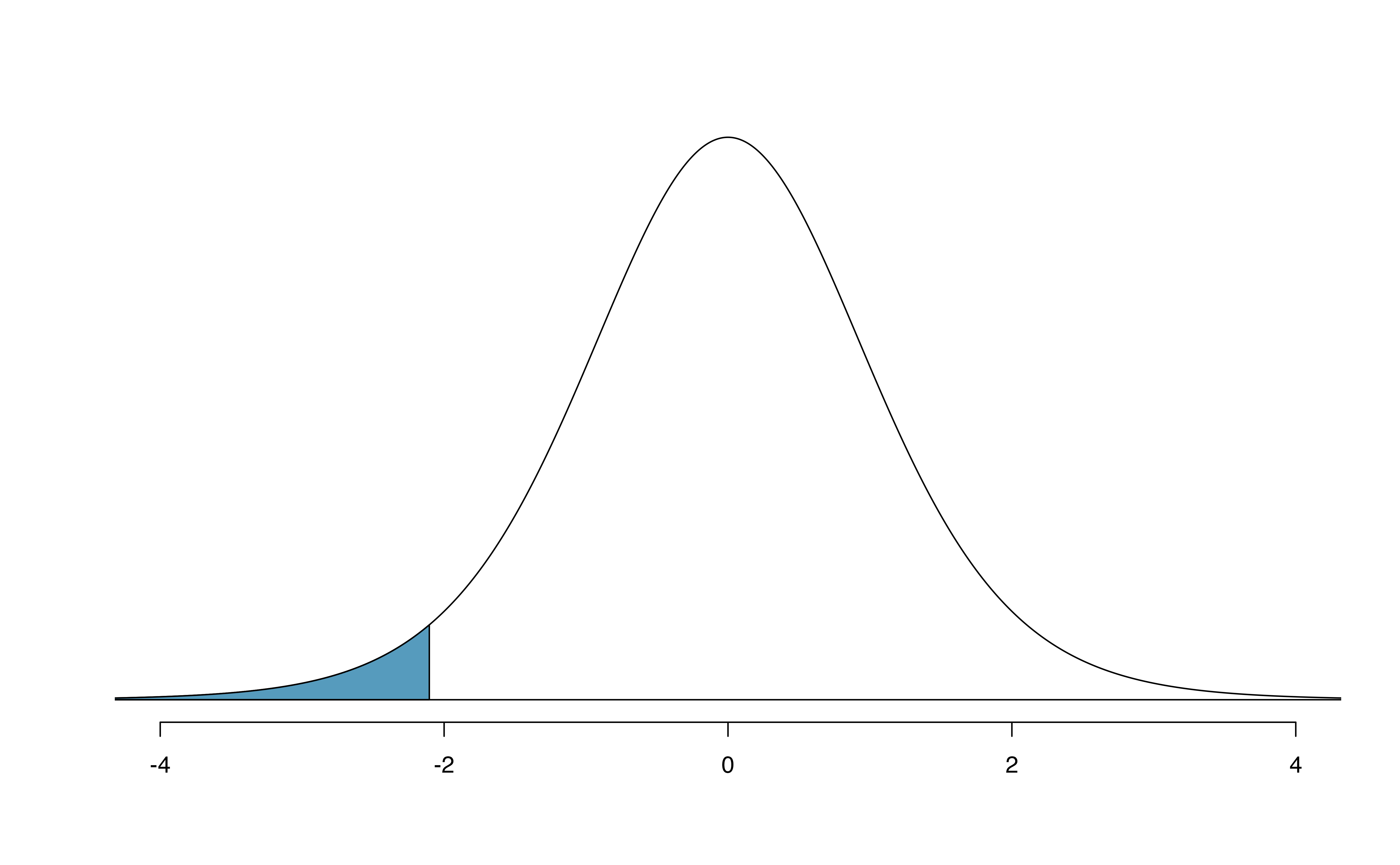

Example 17.2 What proportion of the \(t\)-distribution with 18 degrees of freedom falls below -2.10?

Just like a normal probability problem, we first draw the picture in Figure 17.10 and shade the area below -2.10.

Using statistical software, we can obtain a precise value: 0.0250.

# using pt() to find probability under the $t$-distribution

pt(-2.10, df = 18)

#> [1] 0.025

Figure 17.10: The \(t\)-distribution with 18 degrees of freedom. The area below -2.10 has been shaded.

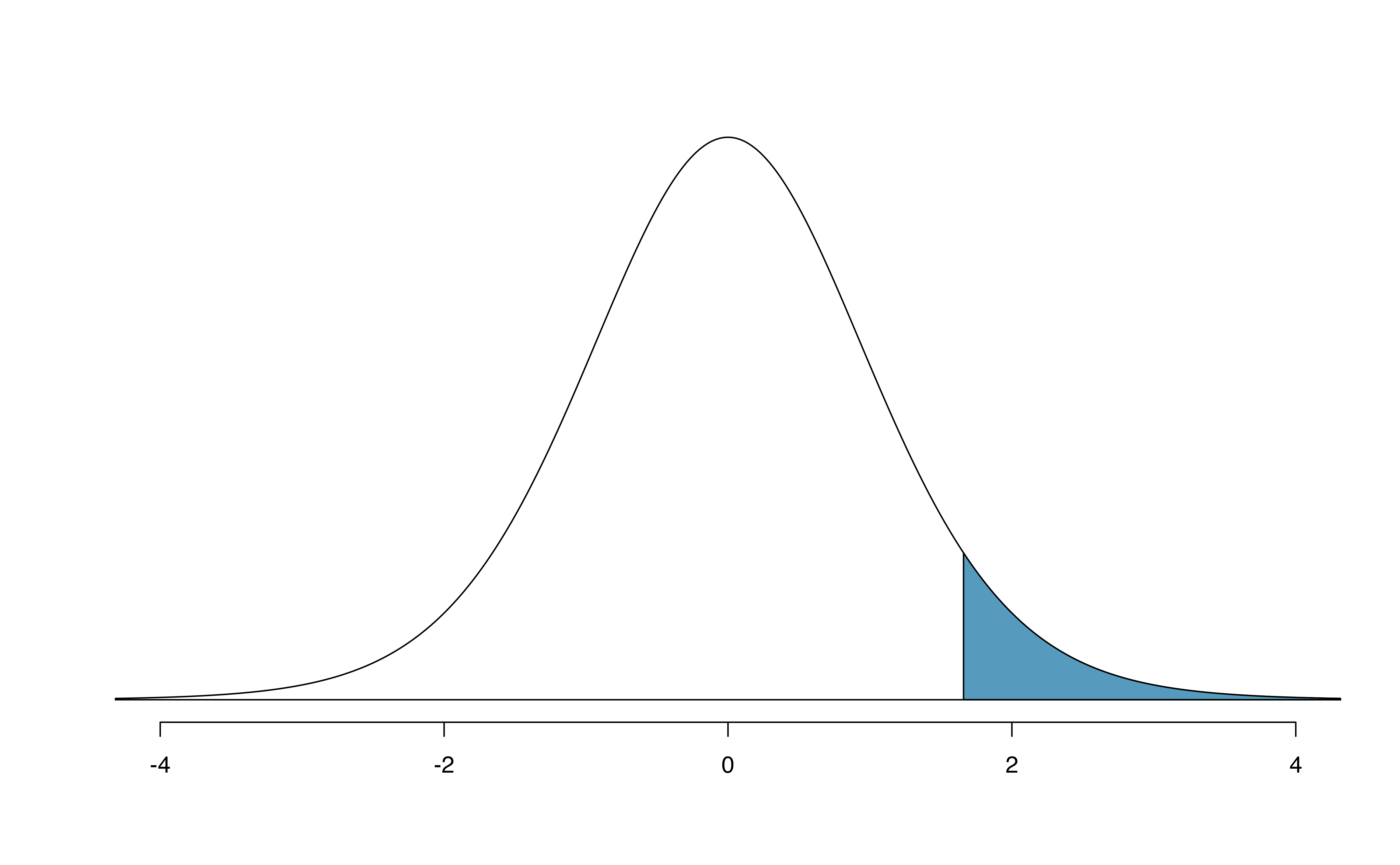

Example 17.3 A \(t\)-distribution with 20 degrees of freedom is shown in the top panel of Figure 17.11. Estimate the proportion of the distribution falling above 1.65.

Note that with 20 degrees of freedom, the \(t\)-distribution is relatively close to the normal distribution. With a normal distribution, this would correspond to about 0.05, so we should expect the \(t\)-distribution to give us a value in this neighborhood. Using statistical software: 0.0573.

# using pt() to find probability under the $t$-distribution

pt(1.65, df = 20, lower.tail=FALSE)

#> [1] 0.0573

# or

1 - pt(1.65, df = 20)

#> [1] 0.0573

Figure 17.11: Top: The \(t\)-distribution with 20 degrees of freedom, with the area above 1.65 shaded. Bottom: The \(t\)-distribution with 2 degrees of freedom, with the area further than 3 units from 0 shaded.

Example 17.4 A \(t\)-distribution with 2 degrees of freedom is shown in the bottom panel of Figure 17.11. Estimate the proportion of the distribution falling more than 3 units from the mean (above or below).

With so few degrees of freedom, the \(t\)-distribution will give a more notably different value than the normal distribution. Under a normal distribution, the area would be about 0.003 using the 68-95-99.7 rule. For a \(t\)-distribution with \(df = 2\), the area in both tails beyond 3 units totals 0.0955. This area is dramatically different than what we obtain from the normal distribution.

# using pt() to find probability under the $t$-distribution

2 * pt(-3, df = 2)

#> [1] 0.0955What proportion of the \(t\)-distribution with 19 degrees of freedom falls above -1.79 units?145

17.3.3 One sample \(t\)-confidence intervals

Let’s get our first taste of applying the \(t\)-distribution in the context of an example about the mercury content of dolphin muscle. Elevated mercury concentrations are an important problem for both dolphins and other animals, like humans, who occasionally eat them.

Figure 17.12: A Risso’s dolphin. Photo by Mike Baird, www.bairdphotos.com.

Observed data

We will identify a confidence interval for the average mercury content in dolphin muscle using a sample of 19 Risso’s dolphins from the Taiji area in Japan. The data are summarized in Table 17.1. The minimum and maximum observed values can be used to evaluate whether or not there are clear outliers.

| \(n\) | \(\bar{x}\) | \(s\) | minimum | maximum |

|---|---|---|---|---|

| 19 | 4.4 | 2.3 | 1.7 | 9.2 |

Example 17.5 Are the independence and normality conditions satisfied for this data set?

The observations are a simple random sample, therefore independence is reasonable. The summary statistics in Table 17.1 do not suggest any clear outliers, with all observations within 2.5 standard deviations of the mean. Based on this evidence, the normality condition seems reasonable.

In the normal model, we used \(z^{\star}\) and the standard error to determine the width of a confidence interval. We revise the confidence interval formula slightly when using the \(t\)-distribution: \[\begin{align*} &\text{point estimate} \ \pm\ t^{\star}_{df} \times SE(\text{point estimate}) &&\to &&\bar{x} \ \pm\ t^{\star}_{df} \times \frac{s}{\sqrt{n}}, \end{align*}\] where \(df = n - 1\) when computing a one-sample \(t\)-interval.

Example 17.6 Using the summary statistics in Table 17.1, compute the standard error for the average mercury content in the \(n = 19\) dolphins.

We plug in \(s\) and \(n\) into the formula: \(SE(\bar{x}) = s / \sqrt{n} = 2.3 / \sqrt{19} = 0.528\).

The value \(t^{\star}_{df}\) is a cutoff we obtain based on the confidence level and the \(t\)-distribution with \(df\) degrees of freedom. That cutoff is found in the same way as with a normal distribution: we find \(t^{\star}_{df}\) such that the fraction of the \(t\)-distribution with \(df\) degrees of freedom within a distance \(t^{\star}_{df}\) of 0 matches the confidence level of interest.

Example 17.7 When \(n = 19\), what is the appropriate degrees of freedom? Find \(t^{\star}_{df}\) for this degrees of freedom and the confidence level of 95%.

The degrees of freedom is easy to calculate: \(df = n - 1 = 18\).

Using statistical software, we find the cutoff where the upper tail is equal to 2.5%: \(t^{\star}_{18} =\) 2.10. The area below -2.10 will also be equal to 2.5%. That is, 95% of the \(t\)-distribution with \(df = 18\) lies within 2.10 units of 0.

# use qt() to find the t-cutoff (with 95% in the middle)

qt(0.025, df = 18)

#> [1] -2.1

qt(0.975, df = 18)

#> [1] 2.1Example 17.8 Compute and interpret the 95% confidence interval for the average mercury content in Risso’s dolphins.

We can construct the confidence interval as \[\begin{align*} \bar{x} \ \pm\ t^{\star}_{18} \times SE(\bar{x}) \quad \to \quad 4.4 \ \pm\ 2.10 \times 0.528 \quad \to \quad (3.29, 5.51) \end{align*}\] We are 95% confident the average mercury content of muscles in the population of Risso’s dolphins is between 3.29 and 5.51 \(\mu\)g/wet gram, which is considered extremely high.

Finding a \(t\)-confidence interval for a population mean, \(\mu\).

Based on a sample of \(n\) independent and nearly normal observations, a confidence interval for the population mean is \[\begin{align*} \text{point estimate} \ &\pm\& t^{\star}_{df} \times SE(\text{point estimate})\\ \bar{x} \ &\pm\& t^{\star}_{df} \times \frac{s}{\sqrt{n}} \end{align*}\] where \(\bar{x}\) is the sample mean, \(t^{\star}_{df}\) corresponds to the confidence level and degrees of freedom \(df\), and \(SE\) is the standard error as estimated by the sample.

The FDA’s webpage provides some data on mercury content of fish. Based on a sample of 15 croaker white fish (Pacific), a sample mean and standard deviation were computed as 0.287 and 0.069 ppm (parts per million), respectively. The 15 observations ranged from 0.18 to 0.41 ppm. We will assume these observations are independent. Based on the summary statistics of the data, do you have any objections to the normality condition of the individual observations?146

Example 17.9 Calculate the standard error of \(\bar{x}\) using the data summaries in the previous Guided Practice. If we are to use the \(t\)-distribution to create a 90% confidence interval for the actual mean of the mercury content, identify the degrees of freedom and \(t^{\star}_{df}\).

The standard error: \(SE(\bar{x}) = \frac{0.069}{\sqrt{15}} = 0.0178\).

Degrees of freedom: \(df = n - 1 = 14\).

Since the goal is a 90% confidence interval, we choose \(t_{14}^{\star}\) so that the two-tail area is 0.1: \(t^{\star}_{14} = 1.76\).

# use qt() to find the t-cutoff (with 90% in the middle)

qt(0.05, df = 14)

#> [1] -1.76

qt(0.95, df = 14)

#> [1] 1.76Using the information and results of the previous Guided Practice and Example, compute a 90% confidence interval for the average mercury content of croaker white fish (Pacific).147

The 90% confidence interval from the previous Guided Practice is 0.256 ppm to 0.318 ppm. Can we say that 90% of croaker white fish (Pacific) have mercury levels between 0.256 and 0.318 ppm?148

17.3.4 One sample \(t\)-tests

Now that we’ve used the \(t\)-distribution for making a confidence intervals for a mean, let’s speed on through to hypothesis tests for the mean.

The test statistic for assessing a single mean is a T.

The T score is a ratio of how the sample mean differs from the hypothesized mean as compared to how the observations vary.

\[\begin{align*} T = \frac{\bar{x} - \mbox{null value}}{s/\sqrt{n}} \end{align*}\]

When the null hypothesis is true and the conditions are met, T has a \(t\)-distribution with \(df = n - 1\).

Conditions:

- independently observed data

- large enough sample to satisfy normality

Compare the T score — the standardized sample mean — to the Z score — the standardized sample proportion — presented in Section 14.3. Why do we use a “Z” when standardizing proportions, but a “T” when standardizing means?149

Is the typical US runner getting faster or slower over time? We consider this question in the context of the Cherry Blossom Race, which is a 10-mile race in Washington, DC each spring.

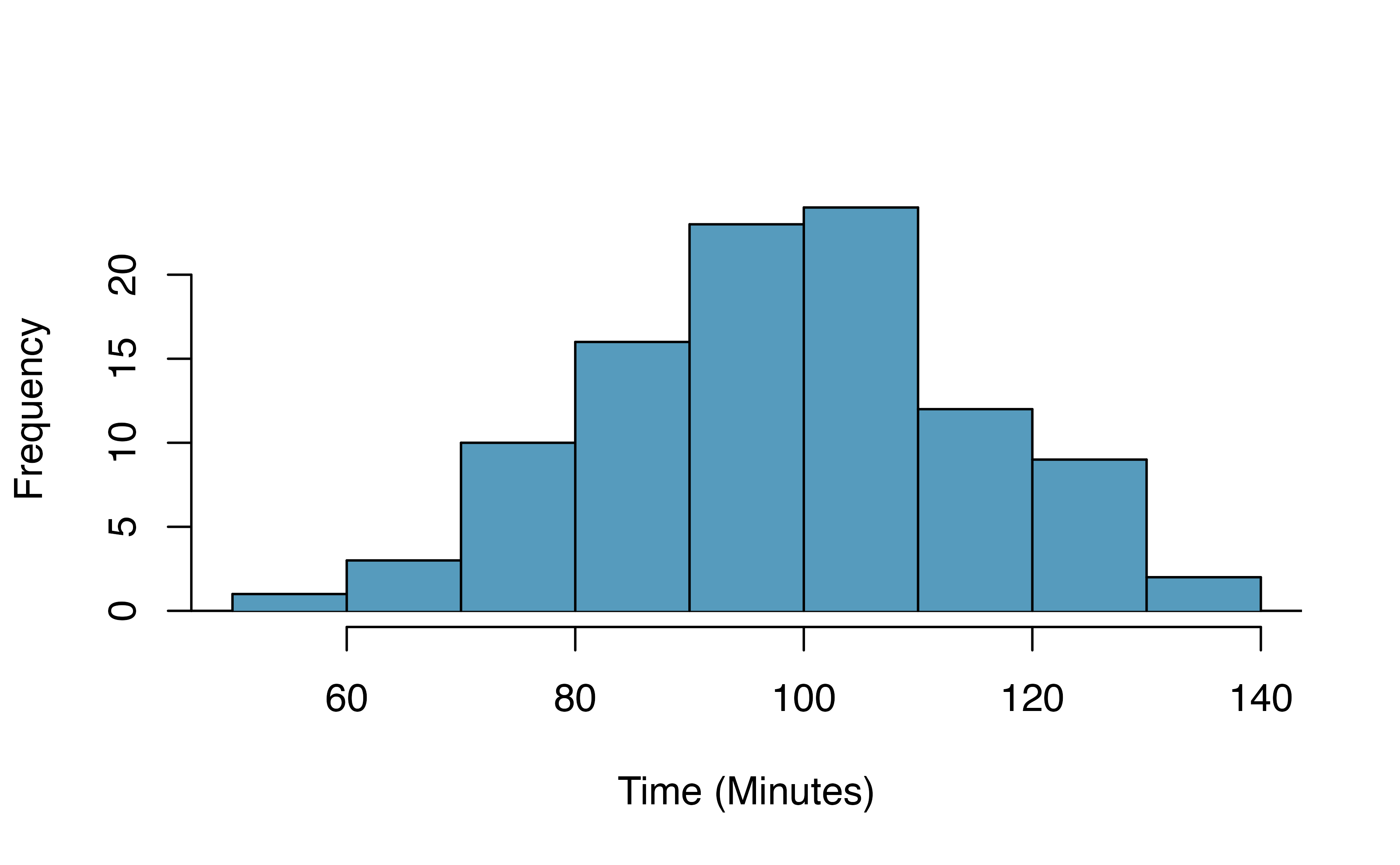

The average time for all runners who finished the Cherry Blossom Race in 2006 was 93.29 minutes (93 minutes and about 17 seconds). We want to determine using data from 100 participants in the 2017 Cherry Blossom Race whether runners in this race are getting faster or slower, versus the other possibility that there has been no change.

What are appropriate hypotheses for this context?150

The data come from a simple random sample of all participants, so the observations are independent.

A histogram of the race times is given to evaluate if we can move forward with a t-test. Should we be worried about the normality condition?151

A histogram of the race times is given to evaluate if we can move forward with a t-test. Should we be worried about the normality condition?151

When completing a hypothesis test for the one-sample mean, the process is nearly identical to completing a hypothesis test for a single proportion. First, we find the Z score using the observed value, null value, and standard error; however, we call it a T score since we use a \(t\)-distribution for calculating the tail area. Then we find the p-value using the same ideas we used previously: find the area under the \(t\)-distribution as or more extreme than our T score.

Example 17.10 With both the independence and normality conditions satisfied, we can proceed with a hypothesis test using the \(t\)-distribution. The sample mean and sample standard deviation of the sample of 100 runners from the 2017 Cherry Blossom Race are 97.32 and 16.98 minutes, respectively. Recall that the sample size is 100 and the average run time in 2006 was 93.29 minutes. Find the test statistic and p-value. What is your conclusion?

The hypotheses, found in a previous Guided Practice, are:

\(H_0: \mu = 93.29\) minutes

\(H_A: \mu \neq 93.29\) minutes

To find the test statistic (T score), we first must determine the standard error: \[\begin{align*} SE(\bar{x}) = 16.98 / \sqrt{100} = 1.70 \end{align*}\] Now we can compute the T score using the sample mean (97.32), null value (98.29), and \(SE\): \[\begin{align*} T = \frac{97.32 - 93.29}{1.70} = 2.37 \end{align*}\] For \(df = 100 - 1 = 99\), we can determine using statistical software that the area under a \(t\)-distribution with 99 \(df\) that is above our observed T score of 2.37 is 0.01 (see below), which we double to get the p-value: 0.02.

Because the p-value is small, the data provide strong evidence that the average run time for the Cherry Blossom Run in 2017 is different than the 2006 average.

# using pt() to find the p-value

1 - pt(2.37, df = 99)

#> [1] 0.00986When using a \(t\)-distribution, we use a T score (similar to a Z score).

To help us remember to use the \(t\)-distribution, we use a \(T\) to represent the test statistic, and we often call this a T score. The Z score and T score are computed in the exact same way and are conceptually identical: each represents how many standard errors the observed value is from the null value.

17.4 Chapter review

Terms

We introduced the following terms in the chapter. If you’re not sure what some of these terms mean, we recommend you go back in the text and review their definitions. We are purposefully presenting them in alphabetical order, instead of in order of appearance, so they will be a little more challenging to locate. However you should be able to easily spot them as bolded text.

| bootstrapping | degrees of freedom | T score |

| Central Limit Theorem | point estimate | t-distribution |